Our Prime minister, Sri. Narendra Modi announced policy support that leads to aatmanirbhar or self-reliant India. They include a rational tax system, simple and clear rules-of-law, good infrastructure, capable and competent human resources, and a strong financial system. While the various organisations and experts have advised on different aspects, let me focus on issues that act as an impediment to achieving this goal. For illustrating the discrimination a case of product supply by three types of supplier is compared – foreign supplier, trader, and MSME. For all three of them, the basic cost is assumed to be 100 units.

The perspective of this article is from an MSME. We all know that MSME is the backbone of any economy and India is no exception. This sector employs more than 111 million people and contributes more than 30% to India’s GDP[1]. In this article, four policies, the discrimination inbuilt in it, and its detrimental impact on MSME are covered.

- Import duty exemption

The first policy is Import duty exemption. The stated objective is to support large industries to reduce their input cost and promote manufacturing. It makes logical sense when there is no alternative MSME supplier in India and only when the final product is made for export.

Let us assess how this policy discourages any kind of technology development and indigenisation in this industry which would have eventually led to aatmanirbhar or self-reliant India.

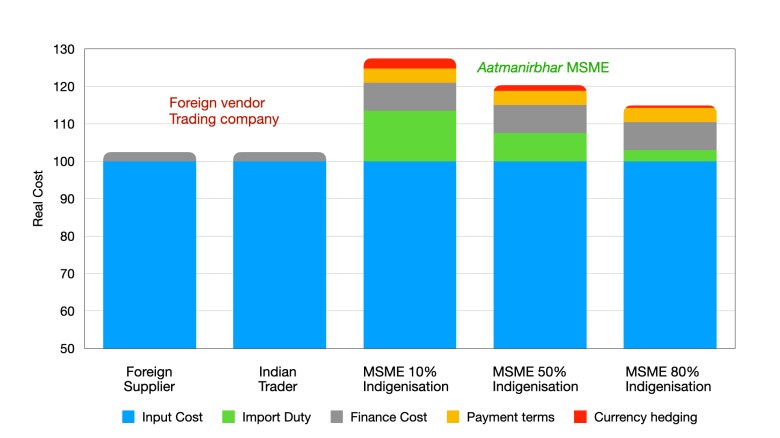

The foreign supplier sells foreign goods. The trader merely imports foreign goods and sells them to the industry. The Indian MSME, following our Prime minister’s call for aatmanirbhar, is planning to indigenise the technology and supply to the industry. Naturally, the firm has to start with a small level of indigenisation and eventually take it to 100%. Let’s assume the various stages at 10%, 50%, and 80%. There is very rarely a high technology product that is 100% indigenous. Let’s see how the large industry treats each of the suppliers and how it incentivises them.

Assume that all three types of firms are equally productive and efficient and their input costs are the same. For 100 units as input costs, let’s look at the real cost due to this policy.

For a foreign firm selling to a large industry or shipyard, since the import duty exemption is in place, there is no additional cost due to import duty and therefore cost remains 100 units. For the Indian trader, again there is no effective import duty since the shipyard will facilitate the high-sea sale and therefore cost remains 100 units.

Now let’s look at the MSME that has started with 10% indigenisation and now aims to reach near 80%. There is no import duty exemption for the components that are imported by this firm, hence 15% basic duty as the additional cost will add up on these 90 units (90% is imported). The additional cost that this MSME has to bear is 13.5 units (15% of 90 units). Assuming that the remaining 10% cost is comparable, the real cost for this MSME is 113.5 units. This MSME would be wondering what would be the cost if it achieves 50% indigenisation. Very simple, it would be 107.5 units and the same cost drops to 103 units when it achieves 80% indigenisation.

The above costs clearly show how the incentive structure works. Shipyards would love a foreign supplier or a trader of a foreign supplier. The moment the MSME thinks of indigenisation their cost shoots up. This will eventually drop to a similar level of the foreign supplier or trader only if MSME achieves close to 100% indigenisation. No doubt that 100% is a great goal, but which firm will take this step if the start is so tough?

- Payment terms

The second policy is payment terms. Policymakers in StartupIndia, MSME thinks that the biggest issue a startup or MSME faces is getting clients. Hence they focus too much on that aspect. They think that by giving exemption on turnover criteria for startups[2] to win a project/tender the problem is solved. They are mistaken. The biggest issue is the financing of the project. The skewed payment terms, especially of Central govt. departments, defence establishments, and PSUs is the bigger problem.

Most of them under various ministries keep the payment terms such that the supplier gets paid 100% after delivery. This becomes an issue mainly when the product is custom built and when it takes a long time like six months to make. The stated objective of this payment procedure is to save the PSUs from the bankruptcy of the supplier or its inability to meet the performance criteria.

In most cases getting the bank to finance the project is the issue and it prevents the startup or MSME from taking up bigger projects. Assume that they manage to get finance, let’s see how it discourages an Indian supplier when compared to the foreign one. The key factor to remember is that Indian MSME gets collateral-free credit at 15% compared to 5% or lower for foreign suppliers. The spread is 10%. Although there are some credit guarantee schemes like CGTMSE[3] the limit is 2 Crore with a close to 10% interest rate. When combined with business loans of 16-18% the average cost of finance is around 15%.

Let’s take the same case of a custom product being supplied. The typical timeline for building a product is six months. Now compare the different suppliers.

For a foreign supplier, the cost of finance is 2.5% of product cost (six months @ 5%), i.e., 2.5 units. A trader who merely acts as a representative of foreign firm is like a foreign supplier. An Indian MSME with ownership of the product and taking the supply risk will have higher finance cost. For such a firm the cost of finance is 7.5% of product cost (six months @ 15%), i.e., 7.5 units.

Clearly, the MSME who thinks of aatmanirbhar is having its competitiveness against foreign suppliers further lowered by this higher finance cost.

In comparison, most state governments and their departments follow stage payments against milestone achievement and there are multiple milestones in a project. At every stage, the payment is slightly lower than the value of the product in that stage to lower risk and also a clause that the part product is the property of the client. This simple measure ensures that both the need for working capital as well as finance cost of the project is lower.

- Difference in Payment timing

The third policy is the difference in payment timing. It is very strange how Central govt. departments, defence establishments, and PSUs get away with differential payment terms between foreign and Indian suppliers.

For a foreign supplier, the payment by Letter of Credit (LC) is made one month before the item is shipped from their factory. The same product if it is made by an Indian MSME, the same government client would make the payment one month after the product is delivered at their store.

In the example of the above product with a six-month timeline for product delivery, there is a three months difference in the timeline between payment to a foreign vendor / Indian trading company versus an MSME manufacturer. Let’s look at the impact on cost. It must be remembered that for an MSME getting financing is the bigger issue. Only if they can manage to get it, the cost of finance become relevant. The additional financing of three months @ 15% is 3.8 units for MSME.

Clearly, the MSME who thinks of aatmanirbhar is having its competitiveness against foreign suppliers further lowered by this difference in payment timing.

- Difference in payment currency

The fourth policy is the difference in payment currency. Let’s look at the terms:

A foreign supplier would be paid in Euro. An Indian MSME will be paid in rupees. An Indian MSME that is trying to indigenise would still have to import components depending on the level of indigenisation. At 10% indigenisation 90% would be imported and so on. To cover the exchange rate risk of the input components, the MSME will have to take currency hedging. It is about 3% for six months of coverage.

Let’s look at the additional cost for the MSME depending on the level of indigenisation. At 10%, they would be importing 90% input materials. The additional cost is 3% of 90 units, i.e., 2.7 units. For MSME with 50% indigenisation the currency exchange cost is 1.5 units and similarly for MSME with 80% indigenisation the cost is 0.6 units.

Now if we add all the costs we get real cost for each supplier.

Real costs

The total spread between a foreign supplier and an MSME who embarks on indigenisation is 25%. Because of these, and the incentives it generates, govt. departments and PSUs would love a foreign supplier or a trader of a foreign supplier. MSME cannot think of attempting bigger projects. Even if they do, the import duty exemption, payment terms, differences in payment timing, and payment currency would kill their competitiveness. How will aatmanirbhar be achieved with theses rule in place?

[1] MSME Annual Report 2018-19 https://msme.gov.in/sites/default/files/Annualrprt.pdf

[2] Startup India scheme providing exemption to startups on turnover – https://bit.ly/2ZXChpe