Our Prime minister, Sri. Narendra Modi, announced a policy support that leads to aatmanirbhar or self-reliant India. They include a rational tax system, simple and clear rules-of-law, good infrastructure, capable and competent human resources, and a strong financial system. While the various organisations and experts have advised on different aspects, let me focus on issues that acts as impediment to achieve this goal.

The perspective of this article is from an MSME. We all know that MSME is the backbone of any economy and India is no exception. This sector employs more than 111 million people and contributes more than 30% to India’s GDP[1]. In this article, four policies, the discrimination in built and its impact on MSME is covered.

The first policy is Import duty exemption for shipyards. The stated objective is to support Indian shipyards to reduce their input cost and promote shipbuilding. It makes logical sense when there is no alternative MSME manufacturer in India and only when the ship is made for export.

Let’s us assess how this policy discourages any kind of technology development and indigenisation in this industry which would have eventually led to atmanirbhar or self-reliant India. Some shipyards, especially PSU yards, confuse assembling of parts as achieving technology marvel.

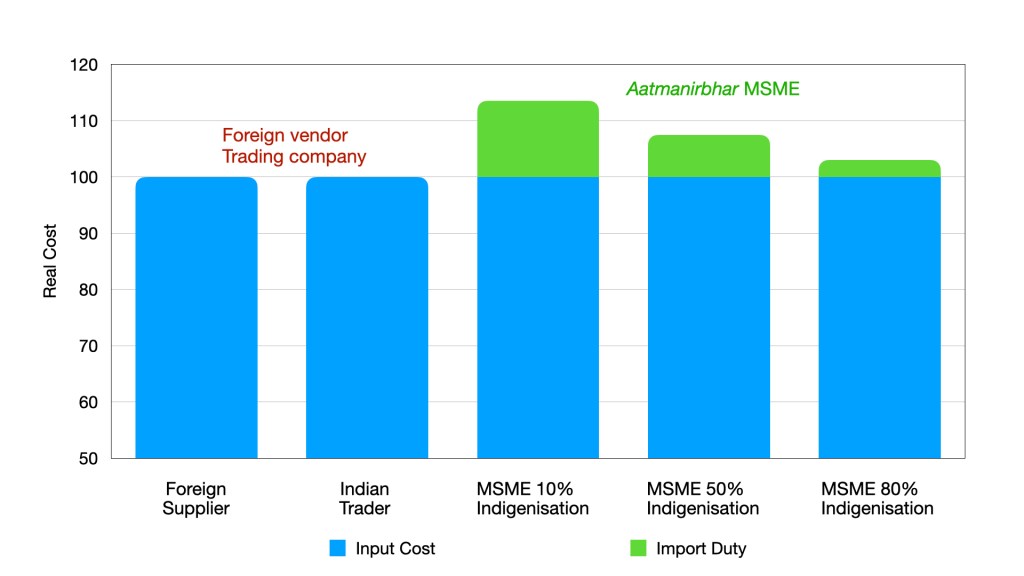

In this example three different types of suppliers of a product is considered – a foreign supplier, an Indian trader and an Indian MSME. The foreign supplier sells the foreign goods. The trader merely imports the foreign goods and sells to the shipyard. The Indian MSME, following our Prime minister’s call for aatmanirbhar, is planning to indigenise the technology. Naturally, the firm has to start with small level of indigenisation and eventually take it to 100%. Let’s assume the various stages as 10%, 50% and 80%. There is very rarely a high technology product that is 100% indigenous. Let’s see how the shipyard treats each of the suppliers and how it incentivises them.

Assume that all three types of firms are equally productive and efficient and their input costs are same. For the sake of simplicity let 100 units be the input cost. Let’s look at the real cost due to this policy.

For a foreign firm selling to a shipyard, since the import duty exemption is in place, there is no additional cost due to import duty and therefore cost remains 100 units. For the Indian trader, again there is no effective import duty since the shipyard will facilitate high-sea sale and therefore cost remains 100 units.

Now let’s look at the MSME that has started with 10% indigenisation and now aims to reach near 80%. There is no import duty exemption for the components that are imported by this firm, hence 15% basic duty as additional cost will add up on this 90 units (90% is imported). The additional cost that this MSME has to bear is 13.5 units (15% of 90 units). Assuming that the remaining 10% cost is comparable, the real cost for this MSME is 113.5 units. This MSME would be wondering what would be the cost if it achieves 50% indigenisation. Very simple, it would be 107.5 units and the same cost drops to 103 units when it achieves 80% indigenisation. Let’s look at it together.

| Foreign supplier | Indian Trader | MSME 10% indigenisation | MSME with 50% indigenisation | MSME with 80% indigenisation |

| 100 | 100 | 113.5 | 107.5 | 103 |

The above char clearly shows how the incentive structure works. Shipyards would love a foreign supplier or a trader of a foreign supplier. The moment the MSME thinks of indigenisation their cost shoots up. This will eventually drop to the similar level of the foreign supplier or trader only if MSME achieves close to 100% indigenisation. No doubt that 100% is a great goal, but which firm will take this step if the start is so tough?

We have seen how import duty exemption for shipyards results in discrimination against MSME vendors. Because of this rule, and the incentives it generate, shipyards would love a foreign supplier or a trader of a foreign supplier. An Indian MSME with some level of indigenisation has higher costs. How will aatmanirbharta be achieved with this rule in place?

Read the second part of this article where discrimination due to finance cost is discussed.

Read the third part of this article where discrimination due to payment timing is discussed.

Read the fourth part of this article where discrimination due to currency difference is discussed.

[1] MSME Annual Report 2018-19: https://msme.gov.in/sites/default/files/Annualrprt.pdf

Sandith,

Big fan of what you do. Aren’t the PSUs inefficient enough to relinquish the input gains and more? In that case, isn’t it better to be you rather than a PSU when you consider overheads? I’m not saying what’s happening right now is how it should be. But I can see you have a lot of strength that they don’t have. Keep up the good stuff!

Cheers,

Sreehari

LikeLike